Economics and markets

A likely China path: Lower but more sustainable growth

October 14, 2021

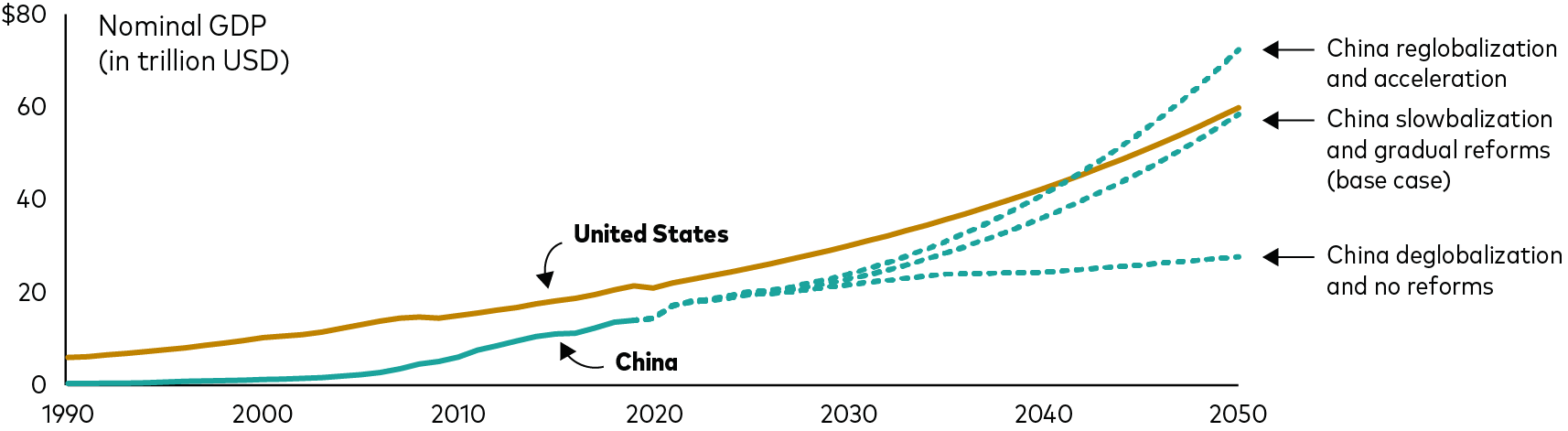

China’s economy has grown since the 1990s from being a tenth of the size of the U.S. economy to close to two-thirds the size.1 This raises some natural questions, including, “When might China become the world’s largest economy?” and “What are the potential portfolio implications of such a new economic order?”

China's future is not a foregone conclusion

Vanguard’s global economics team set out recently to answer these questions and others in the greater context of the world’s productive capacity.

We collected the China-specific findings based on our analysis of nearly 150 countries in A Tale of Two Paths: The Future of China. The paper is part of our Megatrends series, which tries to make sense of how long-term shifts in the global economic landscape are likely to affect the financial services industry and broader society.

We found that China’s future as the world’s largest economy is not a foregone conclusion. Whether China manages to tip the balance of economic power or remains stuck in what is known as the middle-income trap will hinge primarily on its ability to navigate rising international and domestic matters. Continued growth for China could mean portfolio diversification benefits for global investors.

How China could become the world’s largest economy

1As measured by gross domestic product in U.S. dollars.

Sources: Vanguard, using data from the World Bank, as of July 2021.

Our analysis establishes our base case that China’s economy will experience lower but more sustainable growth over the long term as it shifts toward domestic consumption and services, enabling it to outstrip that of the United States sometime beyond 2050.

That scenario factors in headwinds from slowing global trade growth, a trend we looked at recently in another paper in our Megatrends series, The Deglobalization Myth(s). It also anticipates a gradual pace of improvements in education quality, domestic innovation, and privatization reforms, and capital flowing more symmetrically with other nations as policymakers balance a desire for growth rate with medium-term considerations of growth quality and financial stability. Growth could be even faster should reforms and globalization accelerate, allowing China to become the world’s largest economy by 2040.

China’s potential economic trajectories are myriad

The pace and extent of progress in these areas, coupled with an evolving external environment, create multiple potential long-term economic trajectories for China.

Another potential path is that reforms stall and cross-border trade and investment slow sharply, resulting in China’s falling into the middle-income trap—stagnation resulting from a lack of much-needed reform—and failing to ever outstrip the size of the U.S. economy.

China’s transition from the world’s manufacturer to an innovative, consumer-driven economy would have important, uneven spillover effects on global growth. Neighboring countries such as Japan and South Korea would likely benefit from the rise of a Chinese consumer interested in tourism, luxury goods, and education. On the other hand, raw commodity exporters such as Brazil would be hard-hit by a slowdown in China’s old-economy industries such as steel production and manufacturing.

Our outlook for China depends on the path it chooses

Reforms to China's capital markets would likely also have implications for globally diversified investors. China currently has the second-largest equity and bond markets in the world, but a combination of GDP growth, international capital openness, and domestic economic reforms could lead to much greater market capitalizations.

For a globally diversified investor, that could translate into an allocation to China roughly doubling from 7% to 14% in an equity portfolio and 7% to 12% in a bond portfolio by 2035. Allocations to China come with a potential diversification benefit given its relatively low correlation with other markets.

Whether China avoids the middle-income trap depends on the degree to which it undertakes domestic reforms in two interrelated areas: alleviating structural risks related to financial and labor markets and encouraging technological innovation. Its chosen path will define one of the key global economic narratives of a generation.

Notes:

All investing is subject to risk, including the possible loss of the money you invest.

Investments in securities issued by non-U.S. companies and governments are subject to risks including country/regional risk and currency risk.

Diversification does not ensure a profit or protect against a loss.